Hong Kong New Transfer Pricing Laws

Hong Kong's transfer pricing (TP) laws were passed on 04.07.2018 with the Inland Revenue (Amendment) (No. 6) Bill 2017 (Amendment Bill), which comes into force on 13.07.2018. This affirms Hong Kong's commitment to implement OECD's Base Erosion and Profit Shifting (BEPS) initiatives. In the following, Deloitte summaries the important points that businesses should pay attention to as they consider the implications of the changes, and plan for future regulatory compliance.

Hong Kong passes BEPS and Transfer Pricing laws

Hong Kong's Legislative Council on 04.07.2018 passed the Inland Revenue (Amendment) (No. 6) Bill 2017 (Amendment Bill), which comes into force on 13.07.2018 after being signed by the Chief Executive and published in the Gazette. The passing of the Amendment Bill completes the long awaited codification of Hong Kong's transfer pricing (TP) laws, and affirms Hong Kong's commitment to implement OECD's Base Erosion and Profit Shifting (BEPS) initiatives.

The Amendment Bill has been amended since the draft that was issued in December 2017, with a number of amendments made through the Bills Committee Stage, in response to comments received from submitters on the original draft. The Amendment Bill will not be the last word on Hong Kong's TP regulations – the Report of the Bills Committee on this Bill has identified several areas for which further guidance would be issued by the Inland Revenue Department (IRD) through Departmental Interpretation and Practice Notes (DIPN)1 . These are expected to be issued within the coming months, and we will issue tax newsletters on these once they are released.

Our comments below are focused on the key changes since that original draft – as well as important points that businesses should pay attention to as they consider the implications of the changes, and plan for future regulatory compliance.

TP regulatory framework

The Bill codifies Hong Kong's transfer pricing regulations for the first time, and requires that TP regulations in Hong Kong are interpreted in a way that ensures consistency with the OECD TP Guidelines – specifically the 2017 Transfer Pricing Guidelines and Model Tax Convention which incorporate the changes following the BEPS initiatives.

- Hong Kong will adopt the three-tier documentation framework from the OECD BEPS Action 13, bringing formal TP documentation regulations to Hong Kong for the first time. Certain domestic related party transactions will not be subject to the TP regulations. Fewer companies will need to prepare documentation than was originally expected due to relaxation of the exemption threshold introduced during the Bills Committee Stage – further details are provided below.

- Through adoption of the OECD Guidelines, important concepts that were introduced following the BEPS project, such as the alignment of value creation with economic returns, are now part of the Hong Kong TP framework. In particular, Section 15F requires that the entities which perform the DEMPE (i.e. development, enhancement, maintenance, protection or exploitation) activities or deploy the DEMPE assets should be entitled to the associated returns. Taxpayers will need to consider the implications of this concept in situations where contractual obligations may not be entirely aligned with economic value creation. Specifically, taxpayers should turn their mind to whether transactions have been delineated appropriately before considering the preparation of the Hong Kong TP documentation.

- The Bills Committee confirmed that the territorial source principle of taxation will not be changed by the new regulations. Taxpayers should first compute income and profits on an arm's length basis, and then apply the territorial source principle to determine if such income or profits arise in or are derived from Hong Kong. The IRD will provide more guidance in a DIPN.

Transfer pricing documentation

The introduction of formal TP documentation regulations has long been expected for Hong Kong. Implementing TP documentation guidelines in line with BEPS Action 13 ensures consistency for many taxpayers with their international obligations.

The thresholds for preparing documentation have changed since the draft Bill, largely in response to concerns from taxpayers and lawmakers about creating excessive compliance obligations. This has been measured against Hong Kong's intention to maintain a credible and reasonable system that does not draw concerns from the international community on Hong Kong's commitment to the BEPS actions.

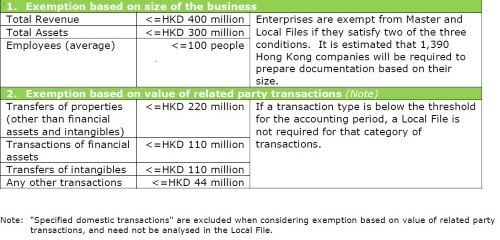

Taxpayers will be exempt from the TP documentation requirements (i.e. preparing Master File and Local File) if they meet the following conditions:

The contents of the Master and Local Files remain unchanged from the draft Bill, and are consistent with the BEPS Action 13. The deadline for preparing the Local File and Master File has been extended from 6 months to 9 months after the accounting year-end, and is aligned with the tax return filing deadline. Experience from the first year of documentation in other jurisdictions is that for the first couple of years this additional time will be essential, especially for companies that have never before prepared TP documentation.

Other matters of interest include:

- The Local and Master Files will only be submitted on request by the IRD. However, taxpayers are required to retain the documentation for 7 years. The IRD will conduct desk audits and reviews to ensure compliance.

- Penalties will apply to taxpayers that do not prepare the documentation on time, from HKD 50,000 to HKD100,000.

- The information gathered by the IRD may be provided to other tax authorities, although the IRD has emphasized that it will only exchange information that is foreseeably relevant to the other jurisdictions, and will not provide information as part of another authority's "fishing expedition".

Country by Country Reporting ("CbC Report")

Hong Kong resident ultimate parent companies of multinational enterprises with consolidated revenue over HKD 6.8 billion in the previous year, or Hong Kong entities that are nominated as surrogate filing entities, will be required to prepare and submit the CbC Report to the IRD. Penalties will apply for nonsubmission, including a HKD 50,000 – HKD 100,000 penalty, plus a daily fine of HKD 500.

Domestic transactions

The Amendment Bill has been amended through the Bills Committee Stage to exempt "specified" domestic related party transactions from the TP rules as well as TP documentation requirements. The changes are set out in Section 50AAJ, which outline that a transaction may not be considered to confer any potential Hong Kong tax advantage if it satisfies the following three conditions:

- The transaction meets the domestic nature test – being a transaction made or imposed in connection with the two parties' trade, profession or business carried on in Hong Kong, or that the transaction is connected with one of the parties' trade, profession or business, and that the other party is a Hong Kong tax resident; AND

- There is no actual tax difference as a result of the arrangement, meaning each person's income (loss) is chargeable (allowable) for Hong Kong tax purpose, and no tax concession or exemption applies to any income (loss); OR the non-business loan test where the lending of money otherwise than in the ordinary course of a money lender or intra-group financing business; AND

- The main purpose, or one of the main purposes, of the transaction is not to utilize any tax loss for tax avoidance purpose.

While the exemption is fairly broad, it is possible that certain domestic transactions may still fall within the TP regulations. Accordingly, Hong Kong taxpayers should study whether their related party arrangements do satisfy all the tests outlined above. Further guidance will be issued by the IRD under a DIPN.

New TP rules related to intellectual property (IP)

The introduction of the OECD's development, enhancement, maintenance, protection, and exploitation ("DEMPE") framework for evaluating the economic ownership of IP brings Hong Kong into line with the latest global standard. Where a Hong Kong taxpayer performs the DEMPE activities / contributes DEMPE assets, but with legal ownership of the IP held by a non-Hong Kong entity, the Amendment Bill introduces specific provision (i.e. Section 15F) to deem the IP-related income to be a taxable receipt of the Hong Kong taxpayer.

IRD will provide more information in a DIPN following the passage of the Amendment Bill, and has deferred the commencement date by 12 months to the year of assessment 2019/20, to allow taxpayers time to prepare.

Permanent establishment

The Bill requires that the Authorized OECD Approach (AOA) be used to attribute income and profits to Hong Kong permanent establishments (PE) according to the Separate Enterprise Principle. The Bills Committee specifically commented that the impact of the AOA on financial institutions was a large part of why the implementation has been delayed by 12 months, to the year of assessment 2019/20.

- Schedule 17G introduces the meaning of a PE in Hong Kong, with different definitions being used for countries with double taxation arrangements (DTA) and those without DTA with Hong Kong. The PE definition for non-DTA countries generally follows the recommendations of the OECD BEPS Action 7, while that for DTA countries would follow the PE articles of the existing DTAs with Hong Kong.

- The AOA gives the IRD the power to assess a Hong Kong branch of a foreign corporation for the income attributed to the branch as if it is a distinct and separate entity. Where a PE in Hong Kong has not previously been explicitly compensated in the past, AOA would allow more income to be attributed to it. With the application of territorial source rules, those onshore sourced profits related to the PE's operations in Hong Kong will be chargeable to Hong Kong tax. In other words, the application of AOA in conjunction with the source rules may result in more profits of the entity being subject to tax in Hong Kong.

- The IRD will issue a DIPN with further guidance for taxpayers – we anticipate that this will provide similar guidance to that issued in other jurisdictions.

Advance pricing arrangement (APA)

The Amendment Bill codifies the APA regime into the Inland Revenue Ordinance, and provides for unilateral, bilateral and multilateral APAs. The IRD will be allowed to charge fees for an APA application based on the hourly rates of the IRD officers involved, subject to a cap of HKD 500,000.

Our observations

This is the first time Hong Kong has introduced TP regulations and documentation requirements, and signals that Hong Kong is committed to implementing the minimum standards under the BEPS initiatives. It is expected that Hong Kong will pay further attention to transfer pricing in the future. The key actions for taxpayers include:

- Reviewing the key related party transactions that may be subject to the new TP regulations as well as TP documentation, and ensuring that support is prepared for any transactions that may be considered as specified domestic transactions.

- Maintaining contemporaneous documentation (e.g. TP policy, inter-company agreements, etc.) to defend the Group's TP position.

- Preparing a gap analysis between the information previously gathered or prepared to support the new TP and documentation requirements, so that information can be prepared in advance of the rules coming into force.

- Watch out for further IRD guidance through DIPNs on some key issues, such as specified domestic transactions, interaction of the new TP rules with Hong Kong's territorial source principle, deeming provision on IP related income, etc.

1DIPNs are issued by the IRD to provide interpretation and guidance in relation to various tax related issues, and are not legally binding.

| www.deloitte-tax-news.de | Diese Mandanteninformation enthält ausschließlich allgemeine Informationen, die nicht geeignet sind, den besonderen Umständen eines Einzelfalles gerecht zu werden. Sie hat nicht den Sinn, Grundlage für wirtschaftliche oder sonstige Entscheidungen jedweder Art zu sein. Sie stellt keine Beratung, Auskunft oder ein rechtsverbindliches Angebot dar und ist auch nicht geeignet, eine persönliche Beratung zu ersetzen. Sollte jemand Entscheidungen jedweder Art auf Inhalte dieser Mandanteninformation oder Teile davon stützen, handelt dieser ausschließlich auf eigenes Risiko. Deloitte GmbH übernimmt keinerlei Garantie oder Gewährleistung noch haftet sie in irgendeiner anderen Weise für den Inhalt dieser Mandanteninformation. Aus diesem Grunde empfehlen wir stets, eine persönliche Beratung einzuholen.

This client information exclusively contains general information not suitable for addressing the particular circumstances of any individual case. Its purpose is not to be used as a basis for commercial decisions or decisions of any other kind. This client information does neither constitute any advice nor any legally binding information or offer and shall not be deemed suitable for substituting personal advice under any circumstances. Should you base decisions of any kind on the contents of this client information or extracts therefrom, you act solely at your own risk. Deloitte GmbH will not assume any guarantee nor warranty and will not be liable in any other form for the content of this client information. Therefore, we always recommend to obtain personal advice. |